Buffett has achieved Berkshire's success by a combination of superior underwriting and investments in companies with durable competitive advantages. However, Buffett himself has cautioned investors about the hindrances of Berkshire's enormous size and the difficulties achieving the same out-sized returns going forward. Also, because Berkshire has a significant number of insurance policies as well as significant investments in many different sectors including banks and manufacturing firms, its portfolio and the company's profits are exposed to risk in the event of prolonged and widespread economic downturn. Warren Buffet's successor as the head of Berkshire after Buffet's eventual departure has not yet been announced, and has caused concern about whether the company will continue to outperform the market.

Business and Financial Metrics

Berkshire typically earns roughly half of its revenue from its insurance businesses, and as such its ability to underwrite efficiently and accurately is critical to its business success. Berkshire's underwriting discipline has led to a negative cost of float (i.e. underwriting gains/losses as a percentage of insurance float). No-cost or negative cost of float allows the company to enjoy investment income and gains without having to pay claims in excess of premiums taken in. In other words, the company operates at an underwriting profit, such that it takes in more in premiums than it pays out in claims. In 2010, Berkshire earned a total of $136 billion in revenues, earning a net profit of $13.0 billion.[1]

Business Segments

Berkshire Hathaway reports earnings from six different segments: i) Insurance earnings, both underwriting profit as well as investment income, ii) Utilities and Energy, iii) Manufacturing, service, and retailing, iv) Finance and financial products, v) Other income, and vi) Investment and derivative gains/losses.

Insurance

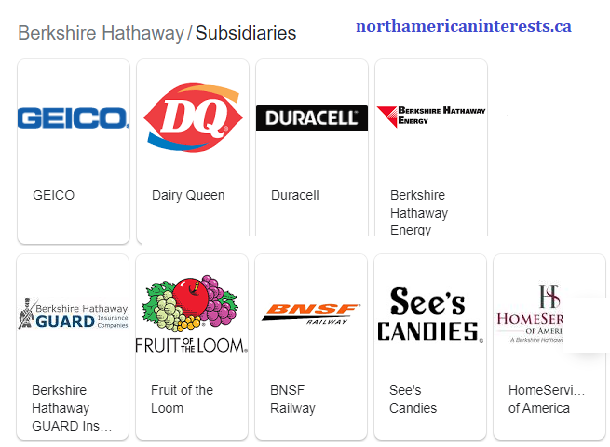

Berkshire Hathaway has four business involved in the insurance and reinsurance businesses: 1) GEICO, 2) General Re, 3) Berkshire Hathaway Reinsurance Group and 4) Berkshire Hathaway Primary Group. The company earns revenues from its insurance business in two ways. First, it can earn an underwriting profit, meaning it collects more in premiums than it pays out. Second, it can invest its float, or money that it receives upfront but has yet to pay out. These two ways are essentially how the insurance business works.

Utilities and Energy

Berkshire Hathaway has a number of utility and energy subsidiaries that make up this segment, most notably which is the MidAmerican Energy Company, which operates an international energy business.

Manufacturing, Service, and Retailing

Berkshire Hathaway owns a number of manufacturing, service, and retail brands from a wide range of industries. Notable companies included in this segment are Marmon Holdings, the McLane Company, Shaw Industries, and a variety of other companies such as Fruit of the Loom, Acme, and many others.

Finance and Financial Products

Berkshire Hathaway's Finance and Financial Products segment is represented by its manufactured housing and and finance business (Clayton Homes). It also performs furniture transportation equipment leasing.

Other Income

The Other Income segment covers the parent holding company and other support subsidiaries that, for the most part, have little or no business activity. These may include legal costs, corporate overhead, etc.

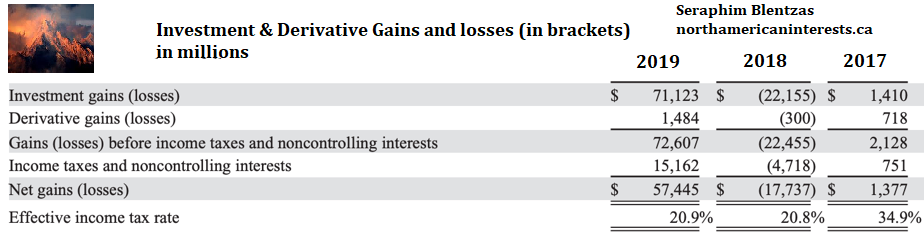

Investment and Derivative Gains/Losses

Investment gains and losses affect Berkshire Hathaway's earnings, but the true impact of these are not felt until they are realized, meaning the actual investment is sold. For example, if Berkshire Hathaway invests in a stock, and the stock price rises, it recognizes a gain, but it has not actually "realized," or gotten the extra cash from the stock price rising until it sells the stock. Only then does the gain become realized and the Berkshire Hathaway actually holds more cash than it paid.

News Updates

On March 14, 2011 Berkshire announced its acquisition of Lubrizol (LZ) for approximately $9 billion. Berkshire is acquiring the company at a 28% premium, and also assuming $700 million in debt from the deal. Lubrizol produces lubricants for large engines such as those found in large trucks, buses and boats as well as airplanes. This investments represents a big bet that Buffett has made on the basic industries.[3] Berkshire is acquiring the company at a 28% premium, and also assuming $700 million in debt from the deal. Lubrizol produces lubricants for large engines such as those found in large trucks, buses and boats as well as airplanes.

Trends and Forces

Warren Buffett as a proven and patient value investor

Buffett's track record as a value investor and sheer financial strength has earned him an incredibly valuable reputation within the financial industry. The value of this reputation can be seen through Buffett's deals with General Electric Company (GE) and Goldman Sachs Group (GS). Both companies came to Buffett, and he came away with very favorable deals in both instances, getting preferred stock that earn a 10% dividend as well as billions in warrants from both companies.[6][7] He was approached first by these companies both because of his reputation as well as the fact that he simply had the funds that most investors did not at the time. Buffett's ability to secure these favorable deals allowed him to profit in times of crisis. In private equity deals, Buffett's reputation also earns him an advantage, as he tends to keep companies together rather than selling off parts of companies.

Because of his long term proven success and fundamental role he plays within Berkshire Hathaway, some Berkshire Hathaway owners have expressed concern about Buffett's succession based on his advanced age. Buffett, 79, has led the capital allocation decisions of the company since present management took over in 1965, and he has announced that the Board of Directors has determined a very short list for a successor CEO. The company intends to split the current CEO role into two roles: CEO (covering operations) and Chief Investment Officer (cover capital allocation and investment decisions). Buffett has indicated that there is a short list of candidates for CIO. Some have speculated that GEICO chief Tony Nicely, reinsurance guru Ajit Jain, or GEICO's investment star Lou Simpson will succeed Buffett as CEO.

Warren Buffett's All In Wager

Berkshire Hathaway completed a deal to purchase Burlington Northern Santa Fe (BNI), the second largest railroad company in the United States for $34 billion in cash and stock.[2] This deal represents the largest in Buffett's career, as he announced the deal is "an all-in wager on the economic future of the United States." As part of the deal, Buffett secured an $8 billion loan from J P Morgan Chase (JPM) and Wells Fargo (WFC), paying somewhere between 1% and 2% above the LIBOR rate.[8] With interest rates at all time lows at the time, many considered this an incredible deal that only Buffett's reputation would afford.

Despite successfully pulling off the deal, the massive deal does not come without potential costs. Berkshire lost its top credit ratings from Moody's (MCO) and Fitch as well as S&P due to the increased debt from the $8 billion loan. Whether the benefits from this deal ultimately outweigh the costs remains to be seen, but this deal will certainly be one of the defining moments of Buffett's career.

Berkshire's massive size limits the potential for outsize returns

Building Berkshire's book value depends on the company's ability to reinvest the large sums of cash flowing into the company and the over $40 billion already in its coffers. The company generates cash flow and float of some $150 million per week,[9] which is typically reinvested in either fixed-income securities, equities, or private companies. As the stock and the flow of cash at Berkshire grows, the company's returns will continue to approach those of the market as it becomes increasingly difficult for Berkshire's to sustain its historical returns of over 20% per year.[10]

Berkshire competes with private equity purchasers for acquisitions of wholly owned subsidiaries

Berkshire's favored investment is in large, privately-held businesses. As such, the company competes with private equity money to find target acquisitions, and increased activity in the space has led to heightened competition and fewer deal opportunities. Berkshire differentiates itself and attracts sellers of businesses by offering them long-term ownership, the hallmark of the company's investment strategy. Often sellers are family or individual owners looking to monetize their interest in a closely-held business. They seek a buyer who, unlike most private equity firms, does not look toward an "exit" of the business and are less likely to interfere with how it is currently managed. Berkshire must maintain its investing track record to continue attracting deals at favorable prices.

Competition

Some competitors of its bread-and-butter insurance operations include State Farm Insurance, Allstate (ALL), Progressive (PGR), Zurich Insurance (ZSA-JO), and Nationwide Corp Group.

Books

MOATS is the best business book that describes the enduring competitive advantages of profitable Berkshire Hathaway businesses. MOATS : The Competitive Advantages of Buffett and Munger Businesses explains the competitive nature of 70 selected businesses purchased by Warren Buffett and Charlie Munger for Berkshire Hathaway Incorporated. This is a very useful resource for investors, managers, students of business around the world. It also looks at the sustainability of these competitive advantages in each of the 70 chapters. The moat is the protective barrier around each business' economic castle. Some of these businesses have double and triple moats of protection.

Footnotes

? 1.0 1.1 BRK 10-K 2010 Item 6 Pg. 28

? 2.0 2.1 Buffett's Berkshire buying Burlington Northern RR. Samantha Bomkamp. BusinessWeek.

? 3.0 3.1 3.2 Buffett bets on emerging markets with Lubrizol buy. Michael Erman. Reuters.

? International Business Times: "Morningstar Names Warren Buffett of Berkshire Hathaway as Its 2008 CEO of the Year" 7 Jan 2009

? Forbes Newsletter Watch "Investment Newsletters Un-Buffetted"

? Buffett boosts Goldman Sachs with $5-billion investment. The LA Times.

? Ron Haruni. Warren Buffett Investing Billions in General Electric. The Wall Street Pit.

? Buffett Cuts Sweet Deal for Burlington Northern Loan. The New York Times.

? Charlie Parker/CBS Interview with Warren Buffett, July 2006

? Forbes Newsletter Watch "Investment Newsletters Un-Buffetted"

berkshire hathaway, subsidiaries, divisions, units, fruit of the loom, duracell, dairy queen, fast food stocks, restaurant chains, diversified portfolio, multinational, investments, geico, warren buffett companies,

Contents

Contents